ToRothorNot | Traditional IRA to Roth Conversion Calculator & Tax Planner

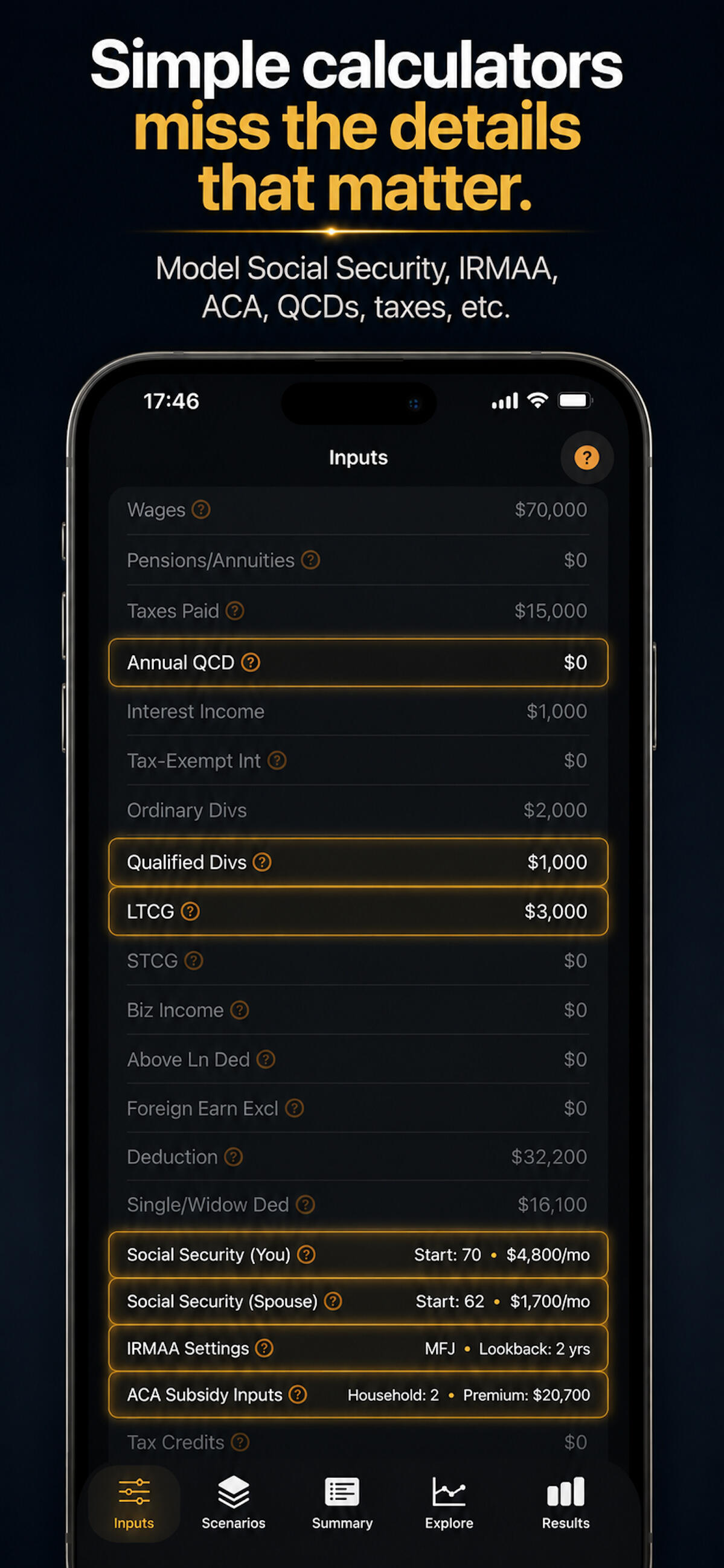

ToRothorNot is a Roth conversion calculator that stands out above the rest. It helps you evaluate whether, when, and how much to convert from a Traditional IRA/401k to a Roth IRA to minimize taxes and maximize net worth. Compare custom scenarios, test Social Security timing, and see how conversions may affect long-term account value, future RMDs, taxes, IRMAA surcharges, ACA subsidies, NIIT, QCDs, survivor-spouse outcomes, and more.

Plan the “gap years” before RMDsThe years before Social Security, Medicare, and required minimum distributions can create important Roth conversion opportunities. ToRothorNot helps you explore those tradeoffs instead of looking only at this year’s tax bill.

Free Version

The free version offers a solid start to help you test some conversion scenarios and compare how they perform over time.

Computed Strategies (Premium)

Computed strategies in the Premium version automatically finds conversion schemes that aim at best end net worth, best net worth at your chosen age, tax bracket fill, and more.

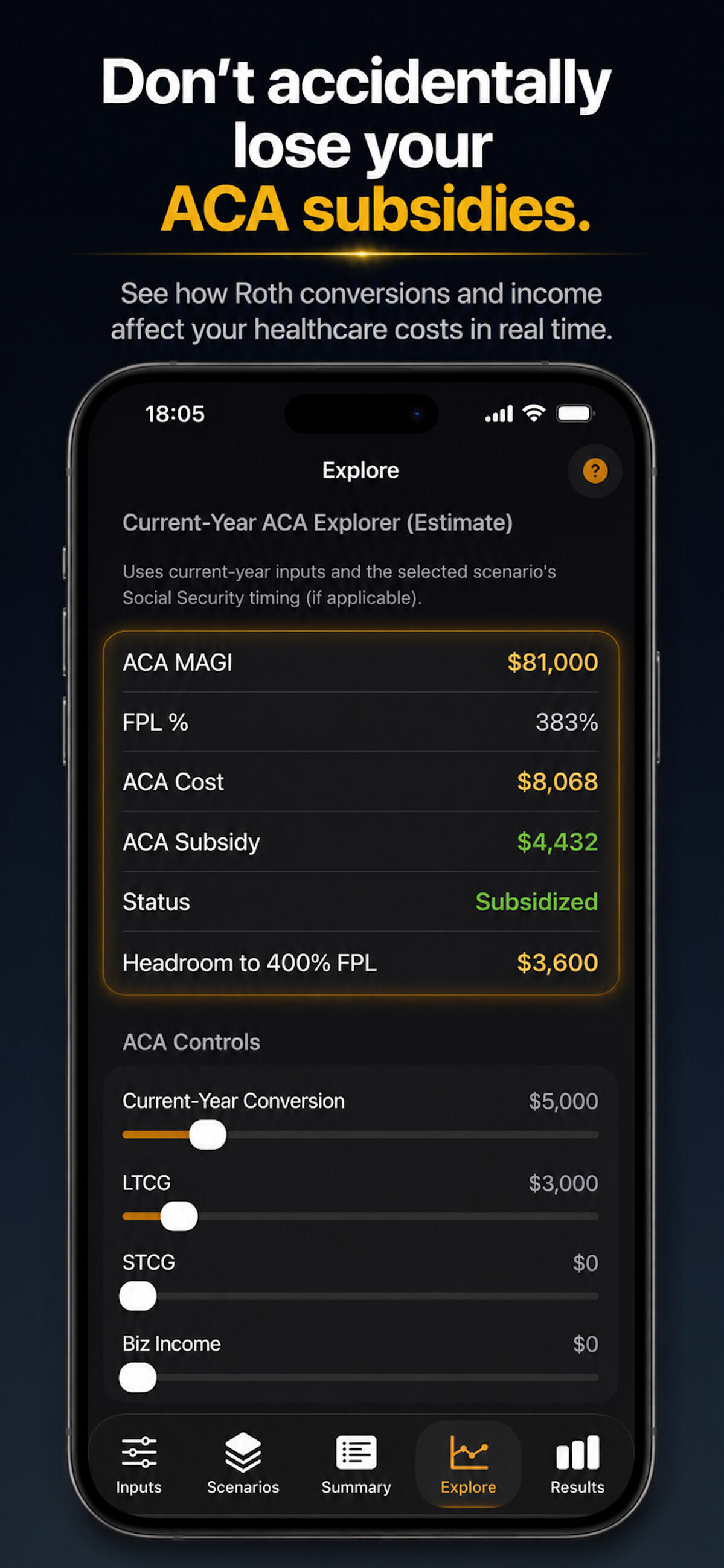

ACA Subsidy Preservation (Premium)

Use ToRothorNot to see how much to convert before driving income too high which could eliminate your ACA/Obamacare Subsidy.

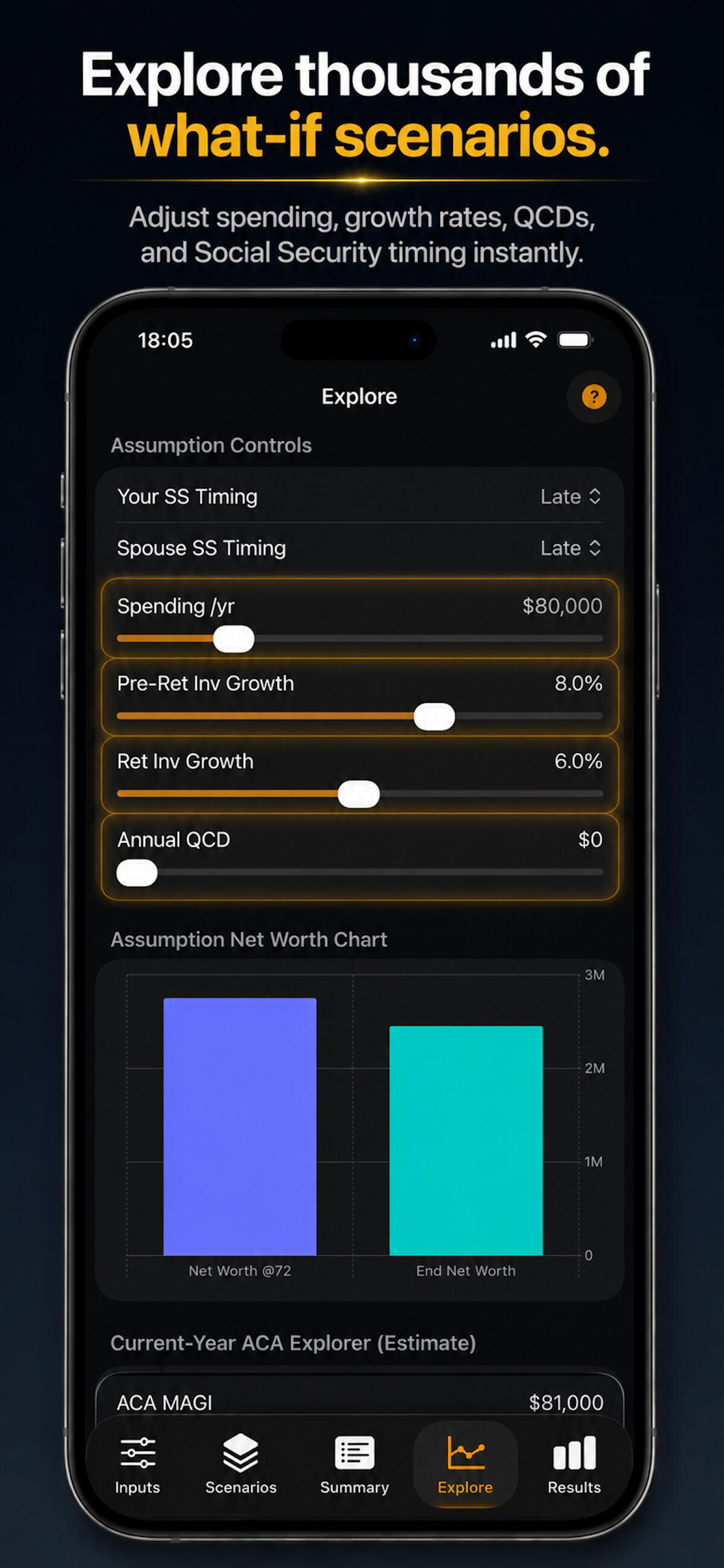

Interactive Explore Tools (Premium)

Dynamically change key inputs like conversion amounts, Social Security timing, spending, growth rate, etc. to see how they impact net worth in real time.

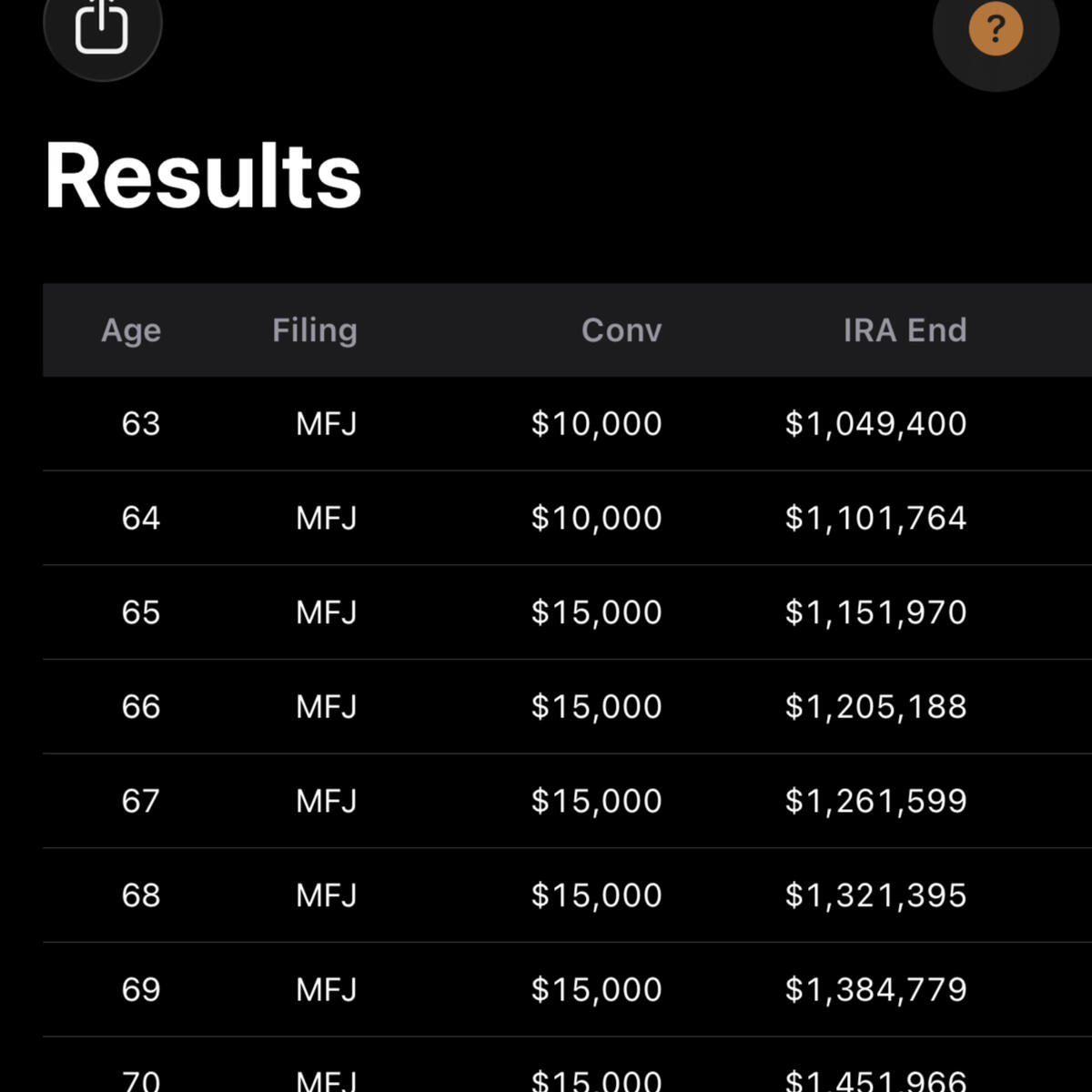

Full Export of Results (Premium)

The Premium version allows full export of results table and a PDF report showing your scenarios and computed strategy results.

Richer Modeling (Premium)

Premium offers deeper and more expansive modeling that takes advanced factors into consideration such as: effect on heirs, survivor results when one spouse passes, qualified charitable distributions, ACA and more.

Why Roth Conversion Timing MattersMany retirement planning decisions depend on timing. The years before Social Security, Medicare, and required minimum distributions (RMDs) may create opportunities for Roth conversions at lower tax rates.A Roth conversion strategy that appears beneficial today may have different results once future tax brackets, Social Security taxation, Medicare IRMAA surcharges, ACA subsidies, capital gains taxes, and survivor-spouse tax rates are considered.ToRothorNot helps you compare these tradeoffs by modeling retirement scenarios over time instead of focusing only on the current year.

App Store, Support, License, and Privacy links below

Frequently Asked QuestionsQ. How is ToRothorNot different from other Roth Conversion Calculators.

A. Other calculators are too simplistic and don't take all key factors into account like Social Security timing, IRMAA surcharges, QCDs, impact to ACA subsidies, widow tax differences, different taxation tables for income, capital gains, Social Security, and more.Q. How different can the results be from ToRothorNot compared to other Roth conversion calculators?

A. Because others are too simplistic, they miss key factors that could

result in a huge difference in taxes paid and net worth over the life of the account owner.Q. Should I do Roth conversions before Social Security?

A. Many retirees and early retirees use the years before claiming Social Security to evaluate Roth conversion opportunities while taxable income may be lower.Q. Can Roth conversions affect Medicare IRMAA surcharges?

A. Yes. Additional income from Roth conversions may increase Medicare IRMAA premiums in future years.Q. Can Roth conversions affect ACA subsidies?

A. Yes. Roth conversions may affect ACA subsidy eligibility and costs for households purchasing health insurance through the ACA/Obamacare marketplace. ToRothorNot will help you model how much to convert (and take as income) before losing your ACA subsidy.Q. Can Roth conversions reduce future RMDs?

A. Reducing Traditional IRA balances through Roth conversions may lower or eliminate future Required Minimum Distributions (RMDs) which lowers your lifetime tax bill and improves lifetime net worth by growing the funds tax-free in the Roth account.Q. Can I compare multiple Roth conversion strategies?

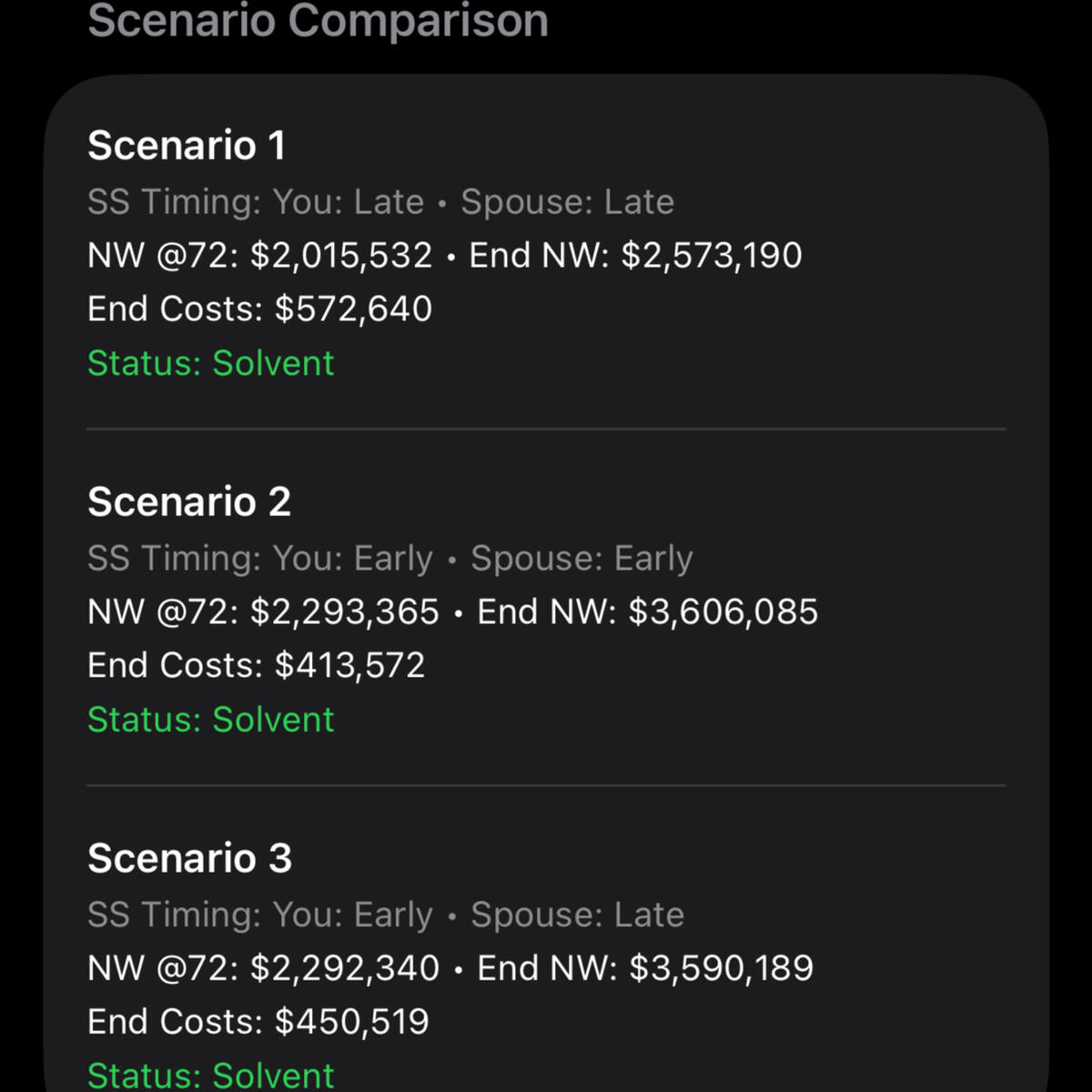

A. ToRothorNot allows side-by-side scenario comparisons and includes automated/optimal scenarios with Premium.

ToRothorNot is an educational planning tool and does not model every IRS worksheet or edge case. It does not guarantee the absolute best strategy will be found, but it can be a practical way to evaluate tradeoffs and prepare for conversations with your professional advisor.

© omSoft LLC. All rights reserved.